Nursing Homes in Mississippi Cost $9,000 a Month. The Asset Limit Is $4,000. And If Your Parent's Income Exceeds $2,982 by a Single Dollar, They're Disqualified — Unless You Know About the Miller Trust.

Your parent needs long-term care. The hospital discharge planner said Medicare's skilled nursing coverage ends soon, and the facility wants a private-pay commitment at $8,500 to $9,000 a month. You've been researching Mississippi Medicaid, but the Division of Medicaid website sends you through layers of PDFs and regional office directories without telling you what to do first. The elder law firms in Jackson and Hattiesburg publish blog posts that all end with a call to schedule a $300-to-$500-an-hour consultation.

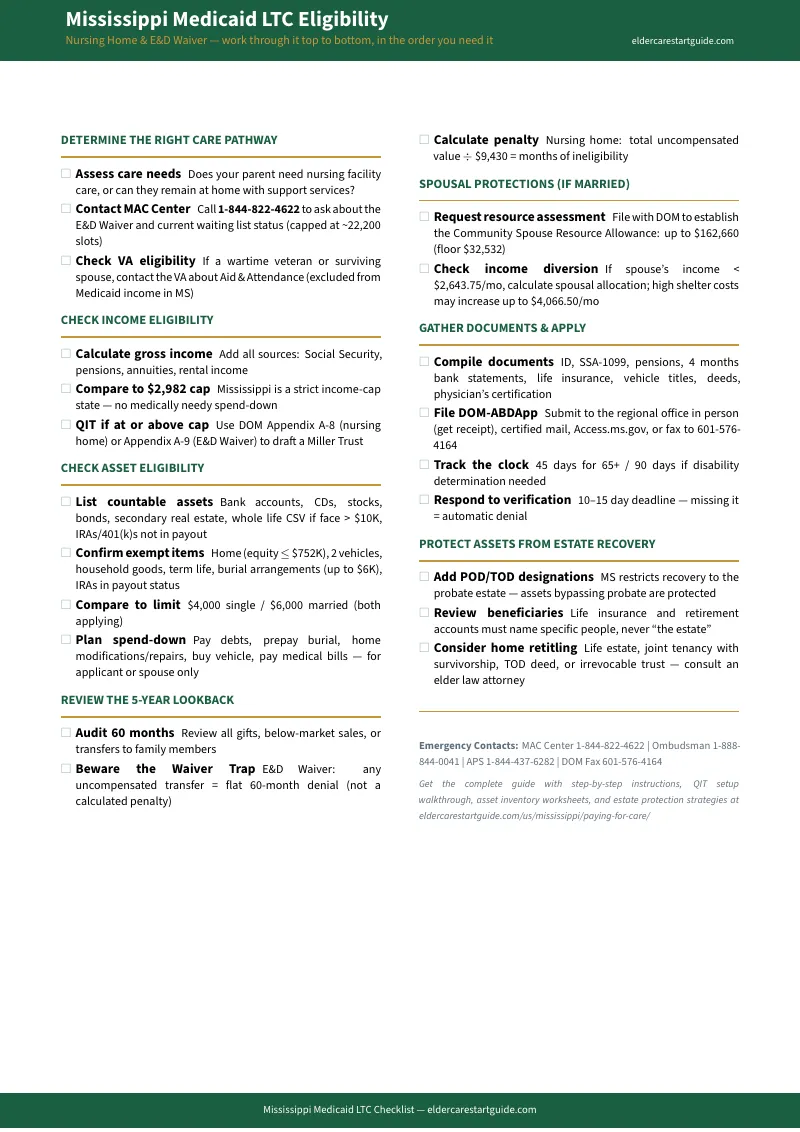

Then you found the financial rules. Mississippi is a strict income-cap state — one of the most rigid in the country. If your parent receives even one dollar above $2,982 per month from Social Security, pensions, and any other source, they cannot qualify for nursing home Medicaid or the Elderly & Disabled Waiver. There is no medically needy spend-down option for long-term care in Mississippi. The only path is a Qualified Income Trust — a Miller Trust — which requires finding a bank willing to open the account, naming a trustee who isn't the applicant, routing all income through the trust every month, and keeping bank fees under the DOM's $10/month cap. Miss any step and the application is denied.

What the discharge planner also didn't mention: the Division of Medicaid uses electronic database matching of Social Security Numbers to verify five years of bank balances and catch every uncompensated transfer. A gift to a grandchild three years ago, a property sale below market value, money moved to a relative without documentation — any of these triggers a penalty period calculated by dividing the total transferred amount by the $8,500-to-$9,000 monthly private-pay rate. During that penalty period, your family pays out of pocket.

The Mississippi Medicaid Navigation & Asset Protection System

This isn't a summary of DOM rules you could piece together from medicaid.ms.gov, national Medicaid information sites, and elder law blog posts. The Mississippi Medicaid Navigation & Asset Protection System maps the exact sequence of financial assessments, legal decisions, trust setups, and application filings your family needs — starting from wherever you are right now — so you don't lose the family home because you did things in the wrong order.

The critical mistake most Mississippi families make: they start the Medicaid application before resolving the income-cap problem. If your parent's income is above $2,982, the application will be denied on financial grounds regardless of how badly they need care. The guide puts you in the right order: assess financial eligibility first, set up the Miller Trust if needed, organize five years of documentation for the lookback review, execute legitimate spend-down strategies, file the application, and then protect the home from estate recovery after your parent passes.

What You Get

- 12-Chapter Guide (guide.pdf) — The complete Mississippi Medicaid Navigation & Asset Protection System: 2026 income and asset limits, the income-cap trap and why Mississippi is different from spend-down states, Qualified Income Trust setup with bank procedures and trustee responsibilities, countable vs. exempt asset classification, the 60-month lookback with electronic database matching and penalty calculations, approved spend-down strategies, spousal impoverishment protections (CSRA up to $162,660 and MMNA of $4,066.50/month), the Elderly & Disabled Waiver and InterRAI LTSS assessment, the Assisted Living Waiver, application filing through Access.ms.gov or regional offices, essential legal authority (POA and Chancery Court conservatorship), estate recovery defense using Mississippi's probate-only recovery rule, and non-probate titling strategies. Every dollar figure reflects 2026 Mississippi regulations.

- Quick-Start Checklist (Free Download) — 18 actionable items organized across 8 steps: income-cap assessment, asset inventory, Miller Trust setup, lookback audit, spend-down planning, application filing, spousal protections, and estate recovery defense. Know exactly what to do tonight, this week, and this month.

- 7 Standalone Printable Worksheets — Ready to print and bring to regional office appointments, bank meetings, and attorney consultations:

- Income & Asset Eligibility Calculator — Audit all income sources against the $2,982 cap, classify assets as countable or exempt, and determine whether a Miller Trust is required

- Spousal Protection Calculator — Calculate the Community Spouse Resource Allowance, determine the Minimum Monthly Maintenance Needs Allowance, and document asset division between spouses

- Five-Year Lookback Audit — Log every transfer from the past 60 months, flag potential penalties, and calculate penalty periods using Mississippi's $9,430 monthly divisor

- Spend-Down Action Planner — Map approved strategies (mortgage payoff, vehicle purchase, home modifications, prepaid burial contracts) with documentation requirements for each

- Estate Recovery Defense Worksheet — Inventory every asset and its current titling, identify which assets would pass through probate, and plan non-probate titling changes (TOD deeds, joint accounts, life estates) to shield them from recovery

- Monthly QIT Distribution Worksheet — Track the required monthly income routing through the Qualified Income Trust for both nursing home and E&D Waiver recipients

- Key Contacts & Forms Reference — Every DOM office, hotline, form number, and 2026 dollar figure on one printable page

Who This Guide Is For

- Adult children in Mississippi whose parent is facing a hospital discharge with Medicare about to run out and a nursing facility quoting $8,500 or more per month in private-pay rates

- Families who know their parent's income exceeds the $2,982 cap and need to understand exactly how to set up, fund, and maintain a Qualified Income Trust before applying

- Community spouses who are terrified that their partner entering a nursing home means losing the family home, their savings, or their monthly income

- Families whose parent needs help at home and want to explore the Elderly & Disabled Waiver as an alternative to facility placement — same financial eligibility rules, same Miller Trust requirement

- Proactive planners who want to organize five years of financial records, execute legitimate spend-down strategies, and retitle assets into non-probate instruments before a care crisis forces rushed decisions

- Out-of-state siblings coordinating a Mississippi parent's care remotely and needing every DOM contact, regional office directory, application pathway, and legal procedure in one reference

Why Free Information Isn't Getting You Anywhere

The Division of Medicaid website publishes eligibility fact sheets, application forms, and regional office addresses. Medicaid Planning Assistance has a Mississippi eligibility page. Brevy Care has income and asset limit summaries. All of this is public, all of it is free, and none of it tells you what to do first.

A Place for Mom and Caring.com rank well on Google, but their business model is referral commissions from private-pay facilities — often the first month's rent. They are structurally incentivized to steer your parent toward expensive placement, not to help you qualify for Medicaid or set up a Miller Trust. They won't walk you through the DOM application process because Medicaid-funded placements don't pay them commissions.

The elder law firms in Jackson, Hattiesburg, and the Gulf Coast publish helpful blog posts about Medicaid planning. Every one ends with a call to schedule a consultation at $300 to $500 per hour. A comprehensive Medicaid planning engagement runs $3,000 to $5,000 or more. Their content is designed to generate leads for legal services, not to give you a complete, executable sequence you can follow yourself.

This guide fills the gap between the state website that gives you facts without sequence, the law firm that gives you sequence through a multi-thousand-dollar engagement, and the referral site that steers you toward placements you may not need.

Satisfaction Guarantee

If this guide doesn't give you a clear, actionable path through Mississippi's Medicaid, asset protection, and long-term care systems, email [email protected]. We read every message.

— Less Than One Hour of an Elder Law Attorney's Time

Mississippi elder law attorneys charge $300 to $500 per hour. A Chancery Court conservatorship petition costs thousands in legal fees, court costs, and guardian ad litem expenses. A single procedural mistake — a lookback penalty from an undocumented gift, a Miller Trust filed without the proper trustee designation, a POA executed after your parent lost capacity — can delay Medicaid eligibility by months and cost your family tens of thousands in private-pay nursing home rates.

This guide won't replace an attorney when you need one (and it tells you exactly when that is). But it will save you hours of research, prevent the most expensive mistakes, and ensure you walk into any conversation — with the regional office caseworker, the bank officer opening the QIT account, the Chancery Court clerk, or the elder law firm — knowing exactly what Mississippi law requires.

Download the free Quick-Start Checklist to see the 18 most urgent action items. When you're ready for the complete system, the full guide is waiting.