Your Parent Needs a Nursing Home. Kentucky Says They Make Too Much — And National Websites Say That Doesn't Matter.

Your parent needs long-term care. The nursing home costs nearly $10,000 a month. Their Social Security and pension add up to $3,100. You searched online and found websites claiming that Kentucky is a "spend-down state" — so your parent can qualify by paying down medical expenses. For standard community Medicaid, that is true. For nursing home Medicaid and the Home and Community Based Waiver, it is flatly wrong.

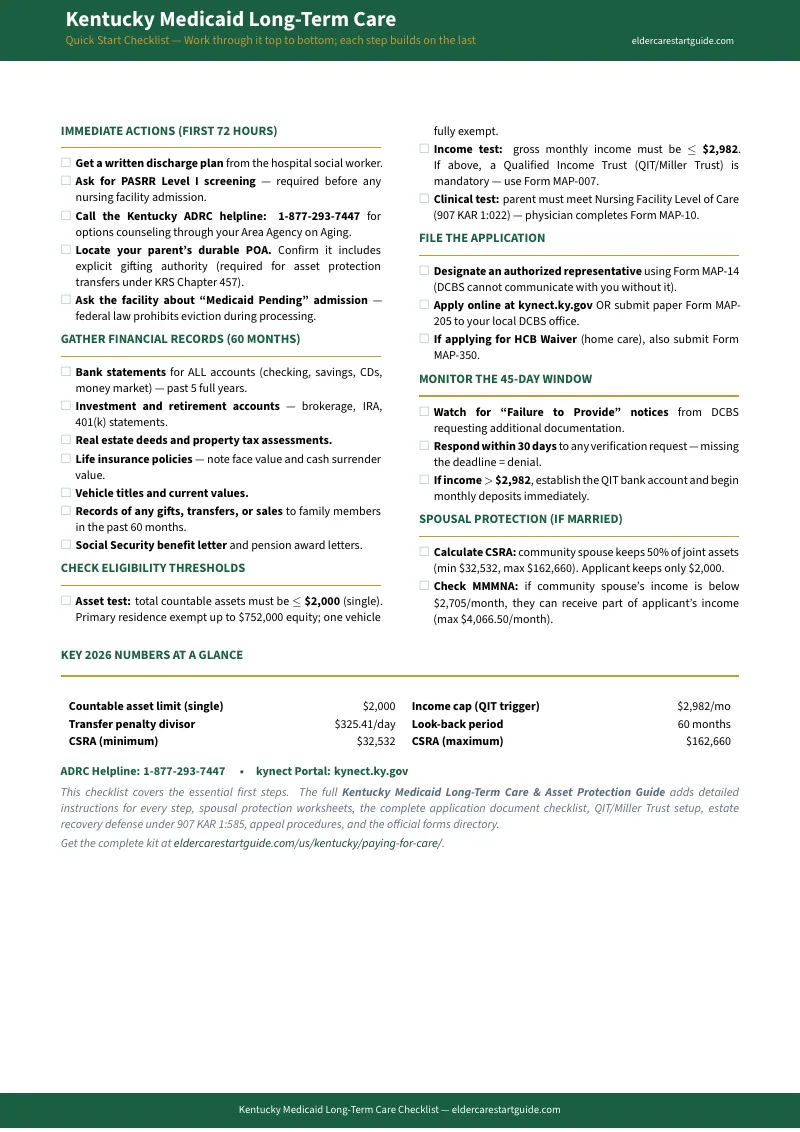

Kentucky enforces a strict Special Income Limit of $2,982 per month for long-term care. Exceed that by a single dollar and your parent is disqualified — unless they establish a Qualified Income Trust using CHFS form MAP-007. No spend-down. No deductible. No workaround except the trust.

You called the Department for Community Based Services. They mentioned kynect, the 60-month look-back, and "countable assets." You logged into the kynect portal and found forms with no instructions. The nursing home is billing your family at the private-pay rate while you try to figure it out. Every week you wait is another $2,500 gone.

The Kentucky Medicaid Asset Protection Playbook

This is not a pamphlet of eligibility limits you can find on a government website. It is the process around the limits — the part that $300/hour elder law attorneys explain in billable consultations and that free government portals never cover.

The guide covers every financial threshold, every legal instrument, every waiver program, and every asset protection strategy available under Kentucky law — organized in the order you will actually need them, from the first hospital discharge through Medicaid approval to estate recovery after your parent passes.

What's Inside

- Qualified Income Trust Setup — Step by Step — Kentucky enforces a hard $2,982/month income cap for long-term care Medicaid. If your parent's gross income exceeds that, they must establish a QIT (Miller Trust) or be denied outright. The guide walks through the trust language required by CHFS form MAP-007, how to open the dedicated bank account, the monthly deposit-and-disbursement cycle ($60 Personal Needs Allowance, then spousal maintenance, then medical expenses, then patient liability), and naming the Commonwealth as remainder beneficiary. Includes the exact distinction between Kentucky's community Medicaid spend-down pathway and the strict income cap for institutional care — because national websites get this wrong.

- Asset Protection Under 907 KAR 1:585 — Kentucky's estate recovery program uses an expanded definition of "estate" that reaches beyond probate — including joint tenancy properties, revocable trusts, life estates, and survivorship deeds. The guide details which ownership structures are vulnerable, which exemptions apply (surviving spouse, minor child, blind or disabled child), the $10,000 administrative threshold below which recovery is waived, and the undue hardship waiver process. Includes specific strategies for protecting the family home during and after a parent's Medicaid enrollment.

- Spousal Protection Formulas — When one spouse enters care, the community spouse keeps between $32,532 and $162,660 in assets under the CSRA, plus a Minimum Monthly Maintenance Needs Allowance of $2,705 (up to $4,066.50 maximum). The guide walks through the Snapshot Date calculation, the Excess Shelter Allowance, and when to request a fair hearing for a higher income allocation — because most families never learn they can ask.

- The 60-Month Look-Back Audit — Kentucky reviews every financial transaction from the past five years. The penalty is calculated using a daily divisor of $325.41 ($9,895.72 monthly equivalent). The guide explains what triggers a penalty (uncompensated transfers), what does not (fair-market-value purchases), and why the IRS $19,000 gift-tax exclusion is a trap — Kentucky Medicaid ignores federal tax code entirely and penalizes the full amount. The penalty clock starts only after admission, not when the gift was made.

- Penalty-Free Spend-Down Strategies — The complete list of Kentucky-approved ways to legally reduce countable assets without triggering a single day of penalty: paying off debts, prepaying irrevocable funeral trusts, making life-safety home modifications, purchasing a vehicle, and paying for home care with a written Personal Care Agreement at fair market value. Every strategy is executable even if your parent is entering a facility tomorrow.

- Home and Community Based Waiver — Kentucky's HCB Waiver allows seniors who meet nursing facility level of care to receive Medicaid-funded services at home. The waiting list exceeds 17,800 people. The guide covers the tiered priority system (Emergency Category for immediate allocation in cases of abuse, neglect, or caregiver death; Urgent Category for allocation within one year), how to apply through your local ADRC or Area Agency on Aging, and how to bridge with private-pay care while waiting for a slot.

- kynect Application Walkthrough — The full application sequence from gathering 60 months of financial records through the kynect portal submission: required documentation (bank statements, income verification, property deeds, vehicle titles, burial trust paperwork), the difference between applying at a DCBS office versus through kynect, when to involve your local ADRC, how to respond to information requests without triggering administrative denial, and the 45-to-90-day processing timeline.

- Legal Authority Chapter — Kentucky's Uniform Power of Attorney Act (KRS Chapter 457), the Health Care Surrogate Act (KRS 311.621–311.643), and the Medicaid-specific clauses your POA must include to interact with DCBS and navigate the kynect system. The full guardianship process through Kentucky District Court when capacity is already gone.

Plus: Printable Worksheets

- QIT Setup Guide — Step-by-step Miller Trust creation: trust drafting per MAP-007, bank account setup, monthly disbursement order, and a ledger template

- Income & Asset Eligibility Calculator — Fill-in worksheet for income and assets against Kentucky's 2026 Medicaid thresholds

- Asset Inventory Worksheet — Map every account, property, vehicle, and insurance policy with countable-vs-exempt status

- Penalty-Free Spend-Down Planner — Tracker for every Kentucky-approved strategy with amounts and completion dates

- Spousal Protection Calculator — CSRA and MMMNA calculation worksheets for married couples

- Five-Year Lookback Audit — 60-month transfer log with penalty calculation using the $325.41 daily divisor

- Estate Recovery Worksheet — Asset vulnerability assessment under 907 KAR 1:585 with exemption tracker

- kynect Application Document Checklist — Every document you need before filing, organized by category

Plus: Printable Quick-Start Checklist

- Kentucky Medicaid LTC Eligibility Checklist — A one-page action list with the 20 most critical items: establish legal authority, gather 60 months of financial records, calculate countable assets, set up the QIT, prepare for the level-of-care assessment, file through kynect. Every threshold, phone number, and deadline at a glance.

Who This Is For

- Adult children whose parent is being discharged from the hospital and someone needs to figure out who is paying nearly $10,000 a month

- Families whose parent's income exceeds $2,982/month and they need a Qualified Income Trust set up correctly — not a template that gets rejected

- Spouses trying to avoid impoverishment when one partner enters a nursing home

- Families who made gifts or transfers in the past five years and need to understand the look-back penalty before it is calculated for them

- Caregivers trying to get a parent onto the HCB Waiver while managing a 17,800-person waiting list

- Out-of-state siblings coordinating Kentucky Medicaid applications remotely through kynect

- Anyone who has been told "it's too late to protect anything" and wants to know what Kentucky law actually allows

Why Not Free Government Resources?

CHFS publishes eligibility limits. Your local Area Agency on Aging offers options counseling. National websites like Medicaid Planning Assistance and Brevy list state-specific thresholds.

Here is what none of them provide:

- A step-by-step QIT setup with the exact language Kentucky requires via CHFS form MAP-007 — not a generic "consult an attorney" note

- The specific asset protection strategies that are legal under 907 KAR 1:585's expanded estate recovery definition, with the exemptions and hardship waiver process

- A complete spend-down strategy list distinguishing penalty-free moves from penalized transfers — including the caregiver agreement template that prevents look-back violations

- The kynect application sequence with the documentation checklist and the information request response protocol

- The critical clarification that Kentucky's community Medicaid spend-down does NOT apply to long-term care — a factual error repeated by multiple national publishers

Government sites administer rules. Elder law firms explain them for $300 to $500 per hour. This guide bridges the gap — translating hundreds of pages of state policy into a sequence you can execute in an evening.

Satisfaction Guarantee

If the guide doesn't give you a clearer path forward, email [email protected] and we'll make it right.

— Less Than One Hour of an Elder Law Attorney's Time

An initial consultation with a Kentucky elder law attorney runs $300 to $500. A full Medicaid planning engagement can cost $3,000 to $5,000. A guardianship proceeding adds thousands more in court costs and legal representation.

This guide won't replace an attorney for complex trust litigation or multi-million dollar estate planning. But for the QIT setup, asset mapping, spend-down documentation, and kynect application process that most Kentucky families need, it covers 90% of the work at a fraction of the cost — and if you do need an attorney, you'll walk in with a fully organized file instead of a box of unsorted bank statements.

Start with the free checklist to see if the approach fits your situation. The full guide goes deeper — every threshold, every strategy, every form, every phone number.