The Hospital Discharge Planner Said Your Parent Is "Alternate Level of Care." Ontario Health atHome Wants a List of Five Homes by Friday. You Have 24 Hours to Accept the First Bed Offer — and No Idea Whether You Are About to Overpay by $800 a Month.

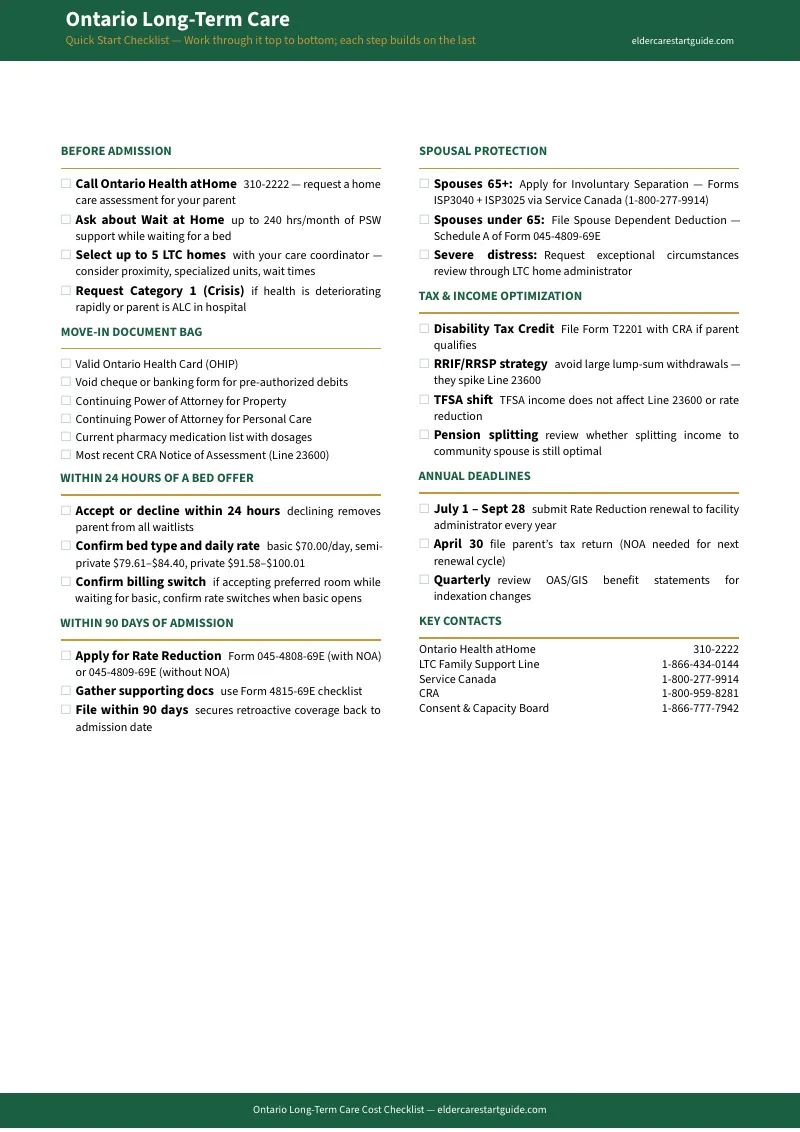

Your parent had a fall, or a stroke, or a cognitive episode that put them in hospital. The medical team stabilized them. Now the social worker says they are ALC — Alternate Level of Care — and the placement process has started. Ontario Health atHome wants your parent's choice list of up to five long-term care homes. Under Bill 7, if you do not cooperate, the placement coordinator can assign a home within 70 km on your behalf. Decline that bed offer, and your parent is removed from all waitlists with a 12-week reapplication ban — or the hospital bills you $70.00 per day in chronic-care co-payment charges.

So you start searching. The Ontario.ca page explains what the co-payment rates are — $70.00/day for basic, $84.40 for semi-private, $100.01 for private — but does not explain how to reduce them. The Ministry website mentions a "Rate Reduction Program" but buries the application behind PDF bulletins written for facility administrators. Your parent's pension income is $1,600 a month. The basic room costs $2,129.17. You have no idea how the gap gets filled, whether the family home is at risk, or what form to file first.

The Ontario Long-Term Care Costs & Subsidies Guide is a Rate Reduction Roadmap — a step-by-step financial toolkit that walks you from the first bed offer through co-payment calculation, Rate Reduction application, spousal income protection, and annual renewal. Not a national elder care overview that treats Ontario as a footnote. Not a $300-an-hour elder law consultation for a process you can handle yourself. An Ontario-specific manual built on the Fixing Long-Term Care Act, 2021, O. Reg. 246/22, and the 2026-27 co-payment rates — covering every form, every deadline, every calculation, and every spousal protection mechanism in the order you actually encounter them.

What's Inside the Rate Reduction Roadmap

An 18-chapter guide, a 20-item quick-start checklist, and standalone printable worksheets — covering every phase of paying for long-term care in Ontario from the first Ontario Health atHome call through annual rate reduction renewal:

The Ontario LTC System Explained — Who Runs What and Who Pays What

Ontario consolidated its home and community care system in 2024. The former LHINs and HCCSS organizations merged into Ontario Health atHome — the single gateway for publicly funded home care and LTC placement. Families who call the old numbers get redirected. Families who search online find outdated references. The guide maps the current system as it operates now: one number (310-2222), one organization, one pathway from home care assessment through facility placement. It explains exactly what the province pays for (all nursing and clinical care) and what families pay for (room and board only), so you know from the start that the co-payment conversation is about accommodation, not medical care.

Home Care Before Placement — What Is Free and Where the Costs Start

Before long-term care, your parent is entitled to publicly funded home care at no cost — personal support workers, nursing visits, rehabilitation therapy — allocated by Ontario Health atHome based on clinical need. But publicly funded hours are strictly capped: no overnight monitoring, no companion care, no 24-hour support. When families supplement with private home care at $25 to $75 per hour, a moderate 20-hour-per-week schedule at $35/hour costs $2,800 per month — more than the basic LTC co-payment of $2,129.17, which includes 24-hour nursing supervision. The guide provides the comparison calculations that help families make this decision with real numbers instead of assumptions.

Co-Payment Rates — The Exact Numbers and How They Change Every Year

The guide publishes the complete 2026-27 rate table: Basic ($70.00/day), Semi-Private ($84.40/day), Private ($100.01/day), plus short-stay respite ($45.31/day). It explains the structural premiums for newer beds (Class A, admitted on or after July 1, 2015) versus older beds (Class B, C, D), and how the annual adjustment works — calculated from the previous year's Consumer Price Index, capped at 2.5%. Every number comes from the Ministry of Long-Term Care bulletin and O. Reg. 246/22, with the exact regulatory references cited.

The Rate Reduction Program — How to Cut Your Parent's Co-Payment

This is the core of the guide. The Rate Reduction Program is Ontario's subsidy for residents who cannot afford the basic accommodation rate. It is available only for Basic beds. It is strictly income-tested — based on Line 23600 (Net Income) of the resident's CRA Notice of Assessment. Assets, investments, and the family home are completely excluded. The program guarantees the resident keeps a $149.00 monthly Comfort Allowance for personal expenses. The guide includes a step-by-step walkthrough of the application (Form 045-4808-69E), a co-payment calculator so you know your parent's adjusted rate before you file, and the exact document checklist you need to assemble.

The 90-Day Window — Why Timing Is Everything

The rate reduction application must be submitted within 90 days of your parent's admission to secure retroactive coverage back to day one. Miss that window and your parent pays the full basic rate for every day between admission and application. The guide maps the 90-day timeline with specific milestones: what to do in the first week, when to request the NOA from the CRA if you do not have it, and how to handle the alternative pathway (Form 045-4809-69E) if no NOA is available — for recent immigrants, non-filers, or residents with foreign income.

Spousal Protection — Two Mechanisms That Keep the Community Spouse Solvent

When one spouse enters long-term care and the other remains in the community, the co-payment can consume most of the couple's combined pension income. Ontario provides two administrative protections. First: Involuntary Separation through Service Canada (Forms ISP3040 and ISP3025), which recalculates OAS and GIS benefits as two single individuals — dramatically increasing the couple's combined monthly cash flow. Second: the Spousal Dependent Deduction (Form 4805-69E), which allows the resident to transfer up to $1,647.04 per month of their income to the community spouse. The guide walks through both mechanisms with annotated sample forms, phone scripts for Service Canada, and calculation worksheets.

Asset Protection — Debunking the American Myths That Cause Panic

Search "long-term care asset protection" and most results come from US elder law attorneys explaining Medicaid's five-year look-back, estate recovery liens, and asset seizure. None of this applies to Ontario. There is no asset test. There is no look-back period. The government will not seize the family home. The Rate Reduction Program evaluates income only — Line 23600 of the CRA tax return. The guide explains exactly how Ontario law protects assets, contrasts it directly with US rules to clear up the confusion, and covers the tax strategies (RRIF withdrawal timing, TFSA shifts, pension splitting adjustments) that keep Line 23600 as low as possible.

Bill 7 and the 24-Hour Bed Offer — A Decision Flowchart

Bill 7 gives Ontario Health atHome placement coordinators the power to assign a home if the family does not cooperate. The 24-hour bed offer window creates intense pressure to accept or decline without understanding the financial implications. The guide includes a printable decision flowchart: what to verify (bed type, rate, geographic location, preferred-room provisional billing), what questions to ask the coordinator, and how to protect your parent's waitlist position for a preferred home while accepting a designated bed in the interim.

Annual Renewal — The Deadline Most Families Miss

The Rate Reduction runs on a July 1 to June 30 cycle. Renewal applications must be submitted between July 1 and September 28 every year. Miss this window and the home is legally permitted to charge the full basic rate immediately. The guide includes a month-by-month calendar with renewal reminders, the exact renewal form, and instructions for handling mid-cycle income changes (such as a parent turning 65 and becoming eligible for OAS/GIS).

Who This Guide Is For

- The adult child who just got the ALC call from the hospital — who has 24 hours to respond to a bed offer under Bill 7 and does not know whether to accept a designated home or risk losing all waitlist positions

- The family watching private home care costs climb past $3,000 a month — who needs a clear financial comparison between keeping a parent at home with paid support and the standardized LTC co-payment that includes 24-hour nursing

- The adult child whose parent's pension does not cover the basic room rate — who needs to know exactly how the Rate Reduction Program works, what form to file, and how to calculate the adjusted co-payment before admission day

- The family protecting a community spouse from financial ruin — who needs the Involuntary Separation and Spousal Dependent Deduction applications explained step by step, with calculation worksheets

- The caregiver who is terrified the government will take the family home — who has been reading US Medicaid advice online and needs to understand that Ontario does not have an asset test, a look-back period, or an estate recovery program for LTC co-payments

Why Free Resources Will Not Get You Through This

The information exists. It is scattered across Ontario.ca PDF bulletins, Ontario Health atHome placement guides, CRA tax instructions, Service Canada pension forms, and the Fixing Long-Term Care Act, 2021. Here is what you actually encounter when you try to navigate the financial side of long-term care using free sources:

- The Ministry of Long-Term Care writes for facility administrators, not families. The co-payment bulletin explains the rate adjustment formula and the CPI calculation methodology. It does not explain how a family with a parent earning $1,600/month on CPP and OAS should fill out Form 4808-69E to get their co-payment reduced from $2,129 to roughly $1,451. That translation is what this guide does.

- Ontario Health atHome coordinates placement but does not advise on finances. Your care coordinator will help you choose homes and manage the waitlist. They will not walk you through the Rate Reduction application, explain the spousal deduction, or advise on tax strategies to keep Line 23600 low. That is outside their scope.

- Commercial senior directories are referral brokers. Comfort Life, A Place for Mom, and similar platforms earn commissions from retirement homes and assisted living facilities. Their content focuses on private-pay options — $3,500 to $6,000/month retirement suites — because that is what generates revenue. Public LTC subsidies get a paragraph, not a chapter.

- US-centric search results create dangerous confusion. Prominent legal directories serve California elder law attorneys to families searching "long-term care asset protection Ontario." US Medicaid advice about five-year look-back periods, Miller Trusts, and estate recovery causes Ontario families to make panicked financial decisions — restructuring assets, transferring property, paying lawyers — for rules that do not exist in this province.

Free resources give you fragments from agencies that do not talk to each other. The Rate Reduction Roadmap puts every Ontario-specific rate, form, deadline, and calculation into one document, in the order you actually encounter them.

— Less Than One Hour With an Elder Law Attorney

An initial consultation with an Ontario elder law attorney runs $300 to $500 per hour. A geriatric care manager charges $100 to $250 per hour. The Rate Reduction application is a standardized administrative process — not complex legal work. This guide costs a fraction of one professional hour and gives you the complete Ontario LTC financial roadmap: the co-payment calculator, the annotated rate reduction forms, the spousal protection worksheets, the Bill 7 decision flowchart, and the annual renewal calendar.

Your download includes the 18-chapter guide, the 20-item quick-start checklist, and standalone printable worksheets you can bring to the LTC home administrator, family meetings, and the CRA:

- Co-Payment Calculator — input your parent's Line 23600 income and see their adjusted monthly co-payment after Rate Reduction

- Rate Reduction Application Walkthrough — annotated Form 4808-69E with field-by-field instructions and common filing errors flagged

- Spousal Dependent Deduction Worksheet — calculate the maximum income transfer to the community spouse

- Involuntary Separation Script — the exact phrasing and form numbers for the Service Canada call

- Bill 7 Decision Flowchart — step-by-step response to a 24-hour bed offer

- Monthly Care Budget Template — track all income sources against co-payment, Comfort Allowance, and optional service fees

- Document Checklist — every paper you need for admission day, the Rate Reduction application, and annual renewal

- Sibling Expense-Sharing Agreement — customizable template for dividing non-subsidized care costs among family members

The process is standardized. The forms are public. What families are missing is the step-by-step sequence that tells them which form to file first, which line on the tax return controls the subsidy, and which deadline — if missed — resets the entire calculation at the full rate.