Your Parent's Nursing Home Costs $16,000 a Month. Connecticut's Asset Limit Is $1,600. Nobody Told You There's a Home Care Program That Protects Thirty Times More.

The hospital discharge planner just told you Medicare's rehabilitation coverage is ending. Your parent can't go home safely. The nursing facility wants $13,863 to $16,000 per month — private pay — and the social worker mentioned something about "spending down" to qualify for HUSKY C Medicaid.

You searched online. You found the number: $1,600. That's Connecticut's countable asset limit for a single Medicaid applicant. Twenty percent lower than the $2,000 federal default that most states use. Your parent has a modest home, a savings account, and a lifetime of careful financial planning. At $1,600, almost everything has to go.

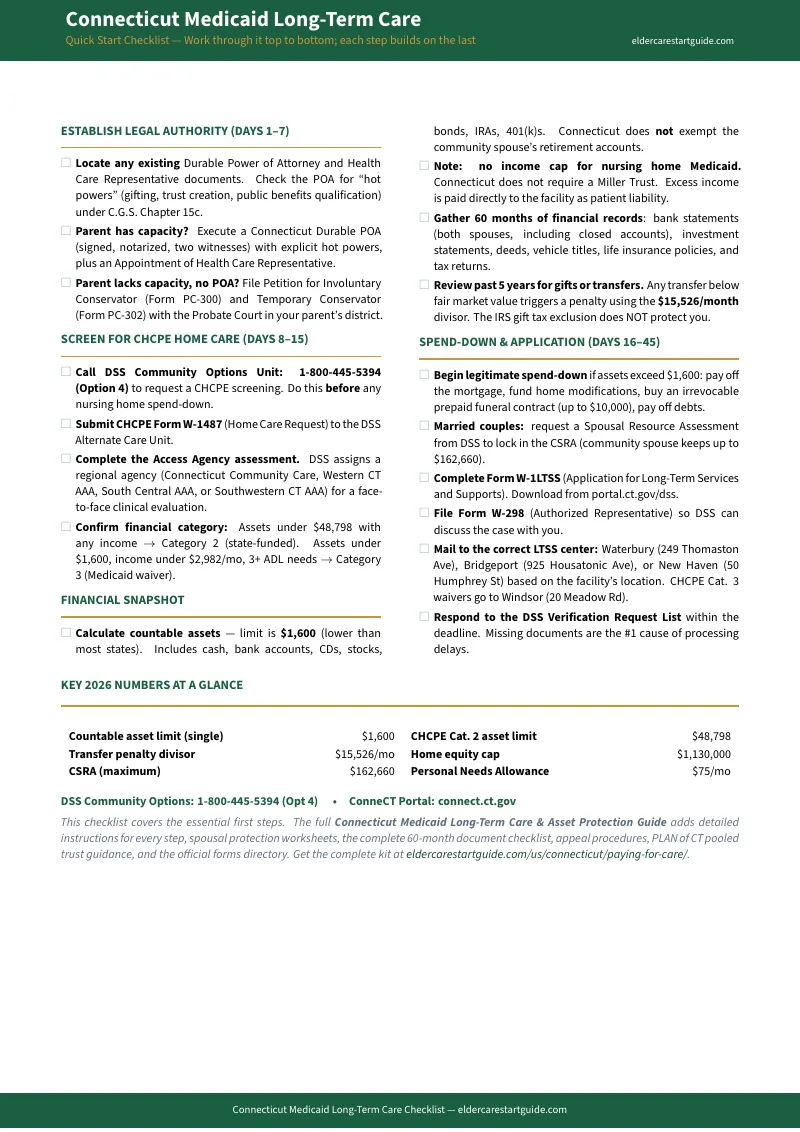

What nobody told you during the discharge scramble: Connecticut operates the Home Care Program for Elders (CHCPE), and its state-funded tier lets your parent keep up to $48,798 in countable assets — with no income ceiling. Screening for CHCPE before committing to a nursing home placement is the single most consequential decision in the entire process. Once your parent enters a facility and the spend-down to $1,600 begins, that protection window closes.

The Connecticut Medicaid Care Navigation System

This isn't a summary of Medicaid rules you could piece together from ten different government websites. The Connecticut Medicaid Care Navigation System maps the exact sequence of decisions, screenings, filings, and deadlines your family needs to follow — starting from wherever you are right now — so you don't burn through your parent's savings because you did things in the wrong order.

The critical mistake most families make: they start the nursing home spend-down before screening for CHCPE. They drain accounts to $1,600 when their parent might have qualified for home care that protects $48,798. They give away money to family members without understanding that the 60-month lookback catches those transfers and imposes a penalty calculated at $15,526 per month of ineligibility. They assume Medicare covers long-term care. It doesn't — not one day of custodial care.

The guide puts you in the right order: screen CHCPE first, understand the asset limits, calculate the patient liability, execute the legal documents while there's still time, then file through the ConneCT portal with everything organized.

What You Get

- CHCPE Screening Blueprint — The step most families skip. Complete walkthrough of Categories 1, 2, and 3: which tier your parent qualifies for, the $48,798 vs. $1,600 asset thresholds, the 9% cost-share copay on state-funded tiers, the functional assessment requirements (two or more ADLs), and how to initiate screening through your Area Agency on Aging before committing to nursing home placement.

- HUSKY C Eligibility Engine — Connecticut's three-part test broken into plain steps: the $1,600 countable asset limit, the Medically Needy spend-down (no income cap — excess income becomes patient liability, not disqualification), and the nursing facility level of care determination. Includes why Connecticut's 209(b) status means national Medicaid guides don't apply here.

- The 60-Month Lookback Audit Prep — Every document the DSS reviews, every transaction caseworkers flag, and every exception that prevents a penalty. Covers the $15,526 penalty divisor, the "trigger date" trap (penalties don't start when the gift was made — they start after your parent has already spent down to $1,600), and the critical rule about joint bank accounts being presumed 100% owned by the applicant.

- Spend-Down Strategy Templates — DSS-approved methods to legally reduce assets to $1,600: paying off the primary mortgage, home accessibility modifications, irrevocable burial contracts up to $10,000, purchasing a vehicle, paying off medical bills and credit card debt. Each method documented with the receipt and record-keeping requirements that prevent caseworker challenges.

- Spousal Protection Calculator — When one spouse enters a facility and the other stays home: how to secure the maximum Community Spouse Resource Allowance (up to $162,660), calculate the Minimum Monthly Maintenance Needs Allowance ($2,643.75 to $4,066.50), and file for a fair hearing if the initial assessment underprotects the at-home spouse. Includes a step-by-step case study with a couple holding $200,000 in joint savings.

- POA vs. Conservatorship Decision Guide — Connecticut's Durable Power of Attorney under CGS § 1-56r requires specific "hot powers" — gifting authority, trust creation, beneficiary changes — that generic online templates don't include. If capacity is already gone, the guide covers the full Probate Court conservatorship pathway: medical evidence, mandatory respondent's attorney, the hearing process, and ongoing court oversight. Side-by-side comparison of cost, timeline, and privacy implications.

- PLAN of CT Pooled Trust Enrollment — Connecticut doesn't recognize individual Miller Trusts. For CHCPE Medicaid waiver applicants whose income exceeds $2,982/month, the only option is a pooled trust managed by the Planned Lifetime Assistance Network of CT. The guide covers enrollment, monthly income flow, and DSS coordination.

- ConneCT Application Walkthrough — Three submission channels (online portal, mail to the Manchester Scanning Center, or in-person at a Regional Resource Center), the Form W-1E navigation guide, the 45-to-90-day processing timeline, retroactive eligibility rules, and the monthly asset deadline. Plus the 90-day Fair Hearing window if the application is denied.

- Estate Recovery Defense — How Connecticut's DSS recovers costs from the probate estate after death, TEFRA lien rules during permanent institutionalization, automatic exemptions (surviving spouse, child under 21, disabled child), the Caregiver Child Exception (two years of in-home care delays placement), and the Undue Hardship Waiver process.

- Quick-Start Checklist (Free Download) — 20 actionable items organized by priority: CHCPE screening, financial document gathering, legal authority assessment, spend-down planning, and application filing. Know exactly what to do tonight, this week, and this month.

- 9 Standalone Printable Worksheets — CHCPE screening worksheet to bring to your AAA appointment, income and asset eligibility calculator, 60-month lookback audit with penalty math, spend-down tracking planner, spousal protection calculator (CSRA and MMMNA), POA vs. conservatorship side-by-side reference, application document checklist with submission addresses, estate recovery worksheet, and patient liability calculator. Print and use each one independently — no need to carry the full guide.

Who This Guide Is For

- Adult children in Connecticut who need to figure out how to pay for a parent's long-term care — nursing home, assisted living, or home care — without losing everything

- Families facing a hospital discharge with no Medicaid application started and a facility demanding private-pay rates of $13,863 to $16,000 per month

- Caregivers who want to keep a parent at home through the CHCPE program but don't know how the screening process works or which tier applies

- Married couples where one spouse needs nursing home care and the other needs to understand exactly how much of their joint savings Connecticut law protects

- Families who made financial transfers in the last five years and need to understand whether those gifts will trigger a Medicaid penalty — and how to document exceptions

- Out-of-state siblings coordinating a Connecticut parent's care remotely and needing every AAA contact, DSS portal instruction, and filing deadline in one place

Why Free Information Isn't Getting You Anywhere

Connecticut's state portals — portal.ct.gov/dss, myplacect.org — provide the raw facts. But they don't tell you the order. They don't tell you that screening for CHCPE before nursing home placement can save $47,198 in protected assets. They don't explain that your parent's joint bank account is presumed 100% theirs for Medicaid purposes, or that the 60-month lookback penalty starts at the worst possible moment — after the money is already gone.

The elder law firms in Fairfield and Hartford counties publish excellent blog posts about Medicaid planning. Every one ends with a call to schedule a $300–$500/hour consultation. Their content is a loss-leader designed to sell legal services, not to give you a complete, executable sequence of steps.

A Place for Mom and Caring.com rank well on Google, but their business model is referral fees from assisted living facilities. They are structurally incentivized to move your parent into a facility, not to help you qualify for state-funded home care that has no referral fee attached.

This guide fills the gap between the government portal that gives you facts without sequence, the law firm that gives you sequence but only through a $2,000–$10,000 planning package, and the referral site that steers you toward placements you may not need.

Satisfaction Guarantee

If this guide doesn't give you a clear, actionable path to paying for your parent's long-term care in Connecticut, email [email protected]. We read every message.

— Less Than One Hour of an Elder Law Attorney's Time

Connecticut elder law attorneys charge $300 to $500 per hour. A comprehensive Medicaid planning package runs $2,000 to $10,000. A single procedural mistake — a transfer penalty triggered by a gift to a grandchild, a CHCPE screening missed before nursing home placement, a POA missing the gifting power your parent's bank requires — can cost $15,526 per month of ineligibility.

This guide won't replace an attorney when you need one (and it tells you exactly when that is). But it will save you hours of research, prevent the most expensive mistakes, and ensure you walk into any conversation — with the DSS, the nursing facility, the Area Agency on Aging, or an elder law firm — knowing exactly what Connecticut law requires.

Download the free Quick-Start Checklist to see the 20 most urgent action items. When you're ready for the complete system, the full guide is waiting.