Michigan Doesn't Allow Miller Trusts — And That Changes Everything About Medicaid Planning

Your parent needs long-term care. Nursing homes in Michigan run $10,000 to $15,000 a month. Medicare's skilled nursing benefit covers rehab for up to 100 days — then the private bill starts. You've been researching Medicaid, but half the guides you find recommend Qualified Income Trusts to handle excess income. Michigan does not recognize or allow them. Following that advice could cost your family months of private-pay bills while you unwind a useless trust and start over.

Michigan operates a "Medically Needy" spend-down system instead of income caps. Clinical eligibility runs through regional Area Agencies on Aging and MI Choice Waiver agencies. Financial eligibility runs through MDHHS county field offices under the Bridges Eligibility Manual. These two tracks operate independently, and families routinely get clinical approval only to face a financial denial months later over an undocumented transfer from three years ago. National guides don't cover this dual-gate system because most states don't have it.

The Michigan Medicaid Navigation System

This guide maps the complete financial, clinical, and legal pathway through Michigan's Medicaid long-term care system — from the Level of Care Determination assessment through the MI Bridges application portal, smart spend-down execution, spousal protections, and post-death estate recovery defense. Every form number, agency name, deadline, and dollar figure is specific to MDHHS and the 2026 Bridges Eligibility Manual.

What separates this from MDHHS fact sheets or law firm blog posts: it connects the systems that Michigan treats as separate processes. Your parent's clinical assessment at the Area Agency on Aging, their financial audit at the county MDHHS office, the MI Choice Waiver waitlist, and the estate recovery claim after death all interact — and filing one step out of sequence can trigger a transfer penalty that leaves your family paying the full private rate for months. The guide shows how these pieces fit together so you can sequence each decision correctly.

What's Inside

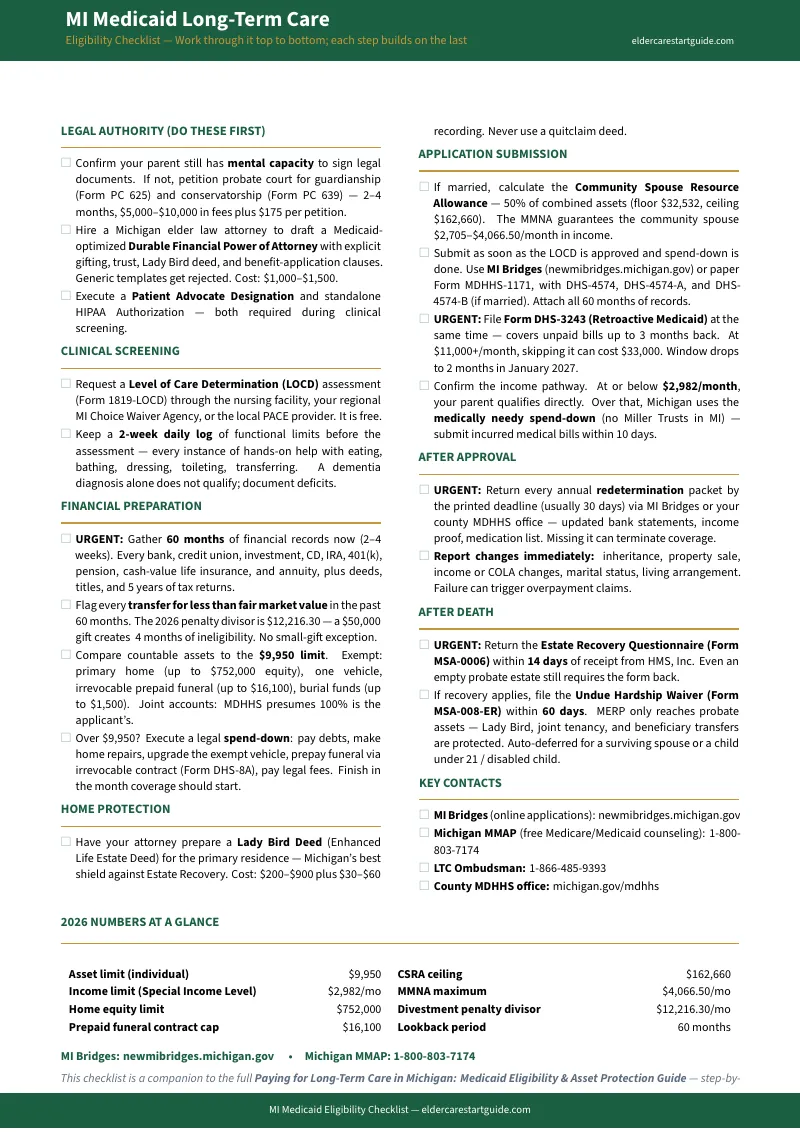

- Income & Asset Eligibility Breakdown — walks through the 2026 numbers ($2,982/month income limit, $9,950 asset limit, $752,000 home equity cap) with Michigan-specific rules for what counts and what's exempt, including how joint bank accounts are treated and why IRAs and CDs are almost always countable

- Medically Needy Spend-Down Calculator — Michigan doesn't use Miller Trusts. If your parent earns over $2,982/month, this section walks through the exact deduction math — incurred medical bills, nursing home charges, and prescription costs submitted within the 10-day window — so you know whether they qualify without hiring an attorney first

- Spousal Impoverishment Protection Planner — calculates the Community Spouse Resource Allowance ($32,532 to $162,660), Monthly Maintenance Needs Allowance (up to $4,066.50/month), and the Excess Shelter Standard ($793/month) so the at-home spouse keeps enough to live on

- 60-Month Lookback Audit Worksheet — maps every gift, transfer, and below-market sale from the past five years and calculates the penalty period using Michigan's 2026 divestment divisor ($12,216.30 per month). No "small gift" exception exists — even birthday money to grandchildren triggers a penalty if it falls inside the window

- Smart Spend-Down Strategy Guide — state-approved methods for converting countable assets to exempt ones (mortgage payoff, home accessibility modifications, vehicle purchase, prepaid irrevocable funeral contracts up to $15,870 plus $1,500 burial fund) with documentation requirements for the BEM 400 caseworker review

- MI Choice Waiver Waitlist Navigation — step-by-step instructions for getting through the regional AAA intake screening, understanding priority categories (Nursing Facility Transitions, Adult Protective Services diversions, Imminent Risk), and the roughly 20,543-slot statewide cap that makes timing critical

- Application Checklist & Filing Guide — every document needed for MDHHS-1171 and the long-term care supplements (DHS-4574, DHS-4574-A, DHS-4574-B), organized in submission order. Covers the MI Bridges online portal, paper filing, and in-person options, plus the retroactive coverage request (DHS-3243) that can recover up to three months of past care costs

- Lady Bird Deed (Enhanced Life Estate) Guide — how Michigan Land Title Standard 9.3 allows your parent to retain full control of the home during life while bypassing probate and shielding it from MERP estate recovery on death. Includes annotated deed language and warns against the quitclaim deed mistake that triggers transfer penalties and kills the tax step-up

- Estate Recovery Defense Worksheet — identifies which assets are exposed through the Michigan probate estate and which bypass it entirely (Lady Bird deed transfers, joint tenancy with right of survivorship, beneficiary-designated accounts). Covers mandatory deferrals, the Estate Recovery Questionnaire, and the 14-day response deadline

- Caregiver Agreement Template Guide — how to structure fair-market-value payments to a caregiving child without triggering a lookback penalty, with documentation requirements that satisfy the BEM 405 divestment audit

Who This Is For

- Adult children whose parent is facing a hospital discharge with Medicare about to run out and no plan for paying the nursing home's $10,000+/month private rate

- Families whose parent earns over $2,982/month and were told they "make too much for Medicaid" — without anyone explaining Michigan's Medically Needy spend-down pathway that bypasses the income limit entirely

- Community spouses terrified of losing the family home or being left with too little income after the institutionalized spouse's patient liability payment takes most of the household money

- Families who found Miller Trust guides online and need to understand what Michigan actually uses instead before filing an application that gets denied

- Proactive planners whose parent is still healthy and want to shelter the home with a Lady Bird deed or irrevocable trust before the 60-month lookback window opens

- Families who transferred property or made gifts to children in the past five years and need to calculate the exact penalty period under the $12,216.30 divisor before applying

- Siblings who need a neutral reference to resolve disagreements about spend-down strategy, whether to pay a caregiving sibling, or when to move from home care to nursing facility placement

Why Free Resources Leave You Stuck

Michigan's MDHHS website and Area Agencies on Aging provide application forms and program descriptions. But their staff are legally prohibited from advising you on asset protection strategy, spend-down sequencing, or lookback penalty mitigation. They can hand you Form MDHHS-1171. They cannot tell you how to restructure your parent's assets to qualify, how to draft a compliant caregiver agreement, or whether your parent's existing power of attorney has the specific clauses needed for gifting, trust transfers, and Lady Bird deed execution.

National publishers like Nolo and AARP build their Michigan pages from templates written for income-cap states. They recommend Qualified Income Trusts — a tool Michigan does not allow. They describe generic life estates — when Michigan's Lady Bird deed operates under its own Land Title Standard 9.3 with specific requirements. Following income-cap state advice in a Medically Needy state creates real financial risk: families set up trusts that MDHHS won't recognize, miss the 10-day medical bill submission window, or fail to file Form DHS-3243 for retroactive coverage.

Elder law attorneys will navigate all of this for you — at $300 to $500 per hour, or $6,500 to $9,500 for comprehensive crisis planning. Using this guide to organize your documents, understand the rules, and identify your parent's specific pathway before that first consultation can save thousands in billable hours. And for families with straightforward applications — no lookback violations, no complex property issues, no guardianship needed — the guide itself is enough.

Satisfaction Guarantee

If the guide doesn't help you identify at least one eligibility pathway, asset protection strategy, or application step you weren't already aware of, email us for a full refund. No forms, no waiting period.

Start Protecting Your Parent's Care and Assets Today

Download the free checklist to get the eligibility overview — or get the full guide for and have every worksheet, calculator, template, and filing reference you need to navigate Michigan's Medicaid long-term care system from first call to approved application.